Natasha

NatashaOver the last few years, Sri Lanka’s economic structure has seen massive change; from being a twin deficit country for decades to suddenly becoming a twin surplus country, and then accelerating along that pathway, which has been astounding in every sense of the word.

Given the positive direction of this change, the positive consequences can be obvious (or at the very least, as long as these conditions continue, the consequences will be obvious).

Perhaps less so would be the costs of such dramatic and rapid change. These costs are not just economic, but also could be institutional, behavioural, and structural in nature, emerging not from the direction of change, but rather from its pace or unevenness.

The challenge lies not in the fact that the country is changing, but that different parts of the economy are changing at different speeds and in varied ways.

Often, rapid improvements in macroeconomic indicators, like what Sri Lanka is currently seeing, can mask the underlying strain or issues that emerge. Systems that were built for and have been operating within a deficit-driven economy are now functioning in a surplus environment, where, as a result, even positive outcomes can generate frictions, as parts of the economy struggle to keep pace with the others.

The biggest place where this change is visible for Sri Lanka is likely in its fiscal performance. Sri Lanka has never maintained sustained fiscal strength, and has definitely never overperformed on that metric. Yet revenue is growing 30% in 2026, even after 2025’s massive growth (and even that was after the huge performance in 2024 and 2023).

Inflation is another area where you see this kind of massive overperformance. After a period of extreme volatility, inflation has now stabilised at relatively low and predictable levels.

Excluding April, which saw a spike in inflation due to the ongoing Middle Eastern conflict and the subsequent rise in fuel prices, over the two-year period between March 2024 and 2026, Colombo Consumer Price Index (CCPI) core inflation has increased by only around 3%, and of this, most has been food prices adjusting for supply factors.

This has provided much-needed breathing space for economic activity, particularly in manufacturing and other trade-related sectors, while also supporting a more stable environment for households and firms. The ability to bring inflation under control and sustain it reflects a level of macroeconomic stability that has been rare in Sri Lanka’s recent history.

Plenty of other areas are also growing dramatically compared to pre-crisis performance, just perhaps a little less than the others. Growth has returned, external balances have strengthened, and overall macroeconomic stability has improved in ways that would have seemed unlikely just a few years ago.

One consequence of the all-encompassing nature of this structural change is that even the ‘weaker’ aspects of this transition are moving extremely fast.

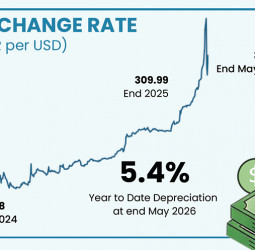

Take reserves, for example. Reserves are only at around the highest they have been at an annual level, but they still managed to get to the highest they have ever been in just three years after reaching zero. That is an absolutely positive performance.

Yet despite that, it is still not as superlative as the fiscal performance has been. This is the fundamental issue here – that you have huge growth (for example, the current account running an external surplus even in March 2026 despite the Iran war), but even this is underperforming in other areas.

One point here is that the gap between what is moving very fast and what is merely moving faster than the rest creates space that needs to be filled. The very fast requires other supporting factors alongside it that the rest of the economy may not be able to provide at the same pace. These ‘missing factors’ are costly.

Institutional capacity, for instance, does not automatically scale with outcomes. As fiscal performance strengthens and the economy becomes more formalised, things like demands on tax administration, regulation, and enforcement also increase significantly. However, these systems take time to adapt and mature, creating short-term mismatches between what is required and what can be delivered in reality.

A similar dynamic is visible within the private sector, where some sectors are able to respond quickly, while others take longer to adapt, creating unevenness in performance across the economy.

As the financial system deepens, it also becomes more central and more complex, creating a novel set of potential risks. Greater reliance on formal financial channels increases interconnections across the economy, placing greater importance on stability, resilience, and risk management.

Events like the recent cybersecurity-related disruption is an indicator that as the system expands and digitises, the scale and impact of such incidents can also grow along with it.

None of these are reasons to slow the transition, but they do underline the need for systems to evolve alongside outcomes. We are seeing enough of these costs already. They are less about clear weaknesses in the system, and more about the nature of an economy in transition, where different parts are moving at different speeds and the overall alignment is still in the process of forming. These costs are probably workable enough, but you still have to face them in the end.

(Damsinghe is the Head of Macroeconomic Advisory and Sumanaweera is a Research Analyst at Frontier Research, a Colombo-based firm that engages in macroeconomic research and advisory for corporate and investment clients on Sri Lanka, South Asia, and Southeast Asia. Damsinghe can be reached at [email protected])

Source: The morning