Tracy

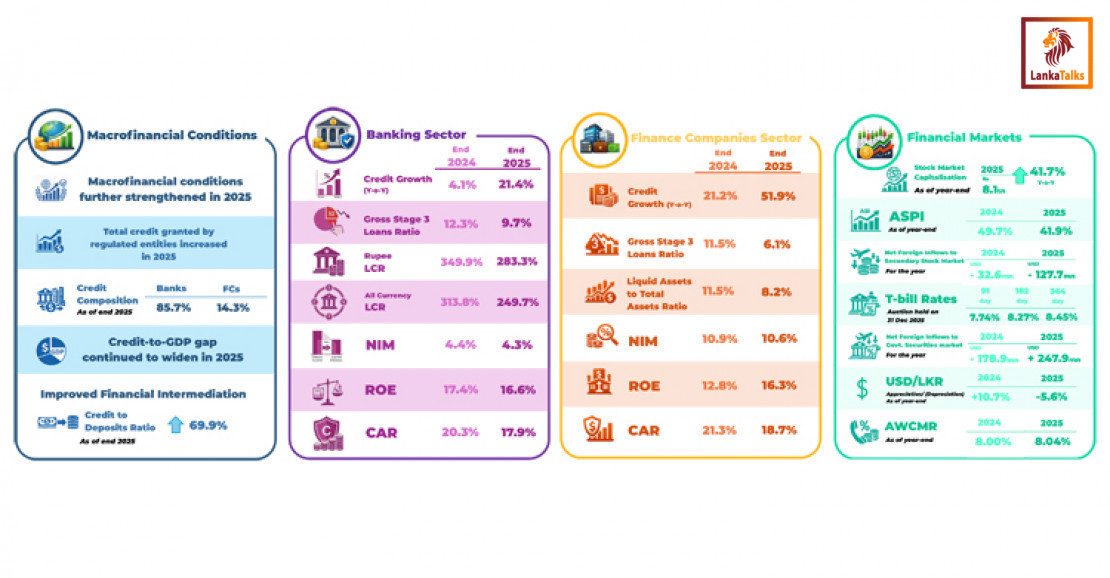

TracyDomestic macrofinancial conditions strengthened further in 2025, supporting continued credit expansion, although external vulnerabilities remained a concern. Credit growth accelerated markedly, with total credit extended by banks and Finance Companies (FCs) rising by end‑2025. The financial sector’s exposure shifted further toward the private sector, driven by strong private sector credit growth, while exposure to the public sector contracted reflecting ongoing fiscal consolidation. Despite the decline, government‑related exposure remains sizeable. Financial intermediation improved, as reflected by the continued rise in the banking sector’s credit‑to‑deposits ratio. However, the credit‑to‑GDP gap widened further into the positive territory of the credit cycle, underscoring the importance of maintaining vigilance over the potential build-up of systemic risk within the financial sector. Global uncertainties, including geopolitical conflict in the Middle East, volatility in commodity prices, and adverse weather conditions, could pose downside risks to credit quality of the financial sector. Against this backdrop, sustained fiscal consolidation and the strengthening of external sector buffers will remain essential to safeguarding macrofinancial stability.

Banking Sector Performance

Credit growth in the banking sector accelerated significantly by end‑2025, supported by accommodative monetary policy, improved macroeconomic conditions, and strong credit demand. Gross loans and receivables expanded by 21.4% year‑on‑year, a substantial increase compared to the 4.1% growth recorded at end‑2024. This expansion was broad‑based, driven by multiple economic sectors including financial services, trade, consumption, lending to overseas entities, construction, and manufacturing. A notable development was the sharp rise in outstanding credit to the financial services sector, which grew by 148.0% year‑on‑year, reflecting increased funding requirements of the FCs sector amid heightened credit demand. Alongside this expansion, the quality of loan portfolios improved, with the stage 3 loans ratio declining to 9.7% at end‑2025 from 12.3% at end‑2024, marking the first return to single digits since the second quarter of 2022.

Reflecting robust credit expansion, liquidity and capital buffers in the banking sector moderated by end‑2025 compared with the previous year, yet remained well above regulatory thresholds. The rupee and all‑currency Liquidity Coverage Ratios (LCRs) declined to 283.3% and 249.7%, respectively, by end‑2025 from 349.9% and 313.8% at end‑2024. Despite this moderation, both ratios stayed comfortably above the minimum requirement of 100%. The sector also continued to demonstrate strong profitability, recording a return on equity of 16.6% in 2025. All banks maintained capital levels above the minimum regulatory requirements, underscoring the sector’s resilience. The total Capital Adequacy Ratio (CAR) stood at 17.9% at end‑2025, compared with 20.3% a year earlier, primarily reflecting the significant credit expansion during the period.

Finance Companies (FCs) Sector Performance

The FCs sector sustained its strong credit expansion momentum by end‑2025, while maintaining resilience in liquidity, profitability, and capital adequacy. Gross loans and advances grew rapidly by 51.9% year‑on‑year at end‑2025, compared with 21.2% growth at end‑2024, underscoring a significant intensification of lending activity. This expansion was driven primarily by vehicle‑backed lending, which increased by 52.7% year‑on‑year, alongside robust growth of 63.8% in gold‑backed lending. Supported by this expansion and improved recoveries, the sector’s gross stage 3 loans ratio declined sharply to 6.1% at end‑2025, from 11.5% recorded at end‑2024. Liquidity conditions remained comfortably above regulatory minimums throughout the year, despite surplus liquid assets decreasing to Rs. 74.3 billion at end‑2025 from Rs. 105.1 billion a year earlier, reflecting accelerated loan disbursements. Profitability strengthened notably, with profit after tax amounting to Rs. 61.5 billion during the first nine months of the 2025/26 financial year[1], marking a significant 45.0% year‑on‑year increase. Meanwhile, the sector’s total CAR moderated to 18.7% at end‑2025 from 21.3% at end‑2024, largely due to the substantial credit expansion.

Performance of Financial Markets

Financial markets remained resilient throughout 2025, supported by improved macroeconomic fundamentals, stable overall market conditions despite geopolitical tensions, and strengthened investor confidence. The Colombo Stock Exchange (CSE) posted strong gains in 2025, with the All Share Price Index (ASPI) and the S&P SL20 Index increasing by 41.9% and 26.6%, respectively, following respective gains of 49.7% and 58.5% in 2024. Market capitalisation also rose sharply, recording a 41.7% increase by end-2025 compared to end-2024. Although a cumulative net foreign outflow of USD 127.7mn was observed during the year, overall market activity remained robust. In the Government securities market, yields remained broadly stable during the fourth quarter of 2025, with a moderate upward adjustment toward late December in line with evolving market conditions. The secondary market for government securities recorded a cumulative net foreign inflow during 2025, largely directed toward Treasury bonds, reflecting improved investor sentiment, although foreign investors continued to hold a relatively small share of total outstanding Government securities. In the foreign exchange market, the Sri Lanka rupee (LKR) continued to adjust in line with prevailing market conditions, depreciating by 5.6% during 2025, following two consecutive years of appreciation, during which the currency strengthened by 12.1% in 2023 and a further 10.7% in 2024. Overall, exchange rate volatility remained contained, and liquidity in the domestic interbank foreign exchange market improved further. In the domestic money market, surplus liquidity persisted throughout the period, contributing to a moderation in short‑term interest rates.

[1] The financial year of the majority of FCs commences on 01 April. However, the financial year of six FCs commences on 01 January. Accordingly, for the purpose of compiling the sector data, the profit after tax of these six FCs for the period starting from 01 April has been considered.

Source: Adaderana