Sheron

SheronSri Lanka should have a 2 percent inflation target with a maximum ceiling of 3 percent which can help people make long-term decisions, save and invest, former Deputy Governor of the Central Bank, W A Wijewardene has said.

Sri Lanka’s central bank has provided exceptional stability to the country since September 2022 with broadly deflationary policy missing its 5-7 percent inflation target, though there are concerns that monetizing bank dollar assets will trigger currency depreciation, unless the rupee defends the ‘borrowed’ reserves.

Sri Lanka has a low inflation rate at around 2 percent a year per annum, according to both the Colombo Consumer Price Index and National Consumer Price Index, Wijewardene said.

“It is a favourable development since such a low inflation will encourage the people to take a long-term view of the economy and save and invest,” Wijewardene said in his column on Sri Lanka’s Daily FT newspaper.

“Such a low inflation rate will help the country to stabilise the exchange rate too. Further, low inflation means low interest rates which are favourable for long term economic development.”

It was wrong to find fault with the central bank for missing a bad target, and bringing about favourable conditions, he said.

“Hence, in my view, instead of seeking to beat the Central Bank on account of its failure to keep up to the target which is undesirable, the Central Bank and the Finance Minister should now sign a new monetary policy framework mandating the Central Bank to achieve a target of 2 percent with a leeway of one percentage point either way.

“Such a target is neutral on the welfare of people since it is compatible with the country’s average productivity growth levels.”

Sri Lanka’s productivity growth appears to be around 2.0 to 2.1 percent, he said.

When the central bank was set up, banks in then Ceylon were buying 20-year government bonds.

With the Federal Reserve yet to start ‘rate cutting’ cycles firing deliberate credit cycles, wild fluctuations in rates leading to ‘market to market’ losses became routine.

But before open market operations spikes in interest rates were rare and largely limited to war time and there was less fear of investing long term.

In 2017 in the midst of World War I, shortly after the Fed was created but before it started open market operations, people in the street bought 30-year Liberty Bonds at 3.5 percent.

The Fed printed money through open market operations (a tactic which was started in April 1923 to run deflationary policy) and created a credit bubble and Great Depression in peacetime in the next decade.

Before the policy rate, and when private central banks were tightly constrained by the gold standard, the British government sold ‘perpetuals’ (no maturity date) which could be bought without fear of steep mark-to-market losses.

Analysts have called for a 2 percent inflation ceiling which will further constrain the central bank and its ability to depreciate the currency and cause social unrest.

Others have also called for an exchange rate target.

Unlike an inflation target which can be manipulated by changing the base after firing currency crises, exchange rates are more transparent and econometrics cannot be used to show lower index inflation.

Many Sri Lankans who used to travel in three wheelers are now using buses and those who used private healthcare are going to state hospitals after the last currency collapse from potential output targeting, which will be reflected in a re-basing based on the latest consumption patterns, analysts say.

Critics of the Fed used to call the phenomenon ‘shifting from hotdogs to dogfood’.

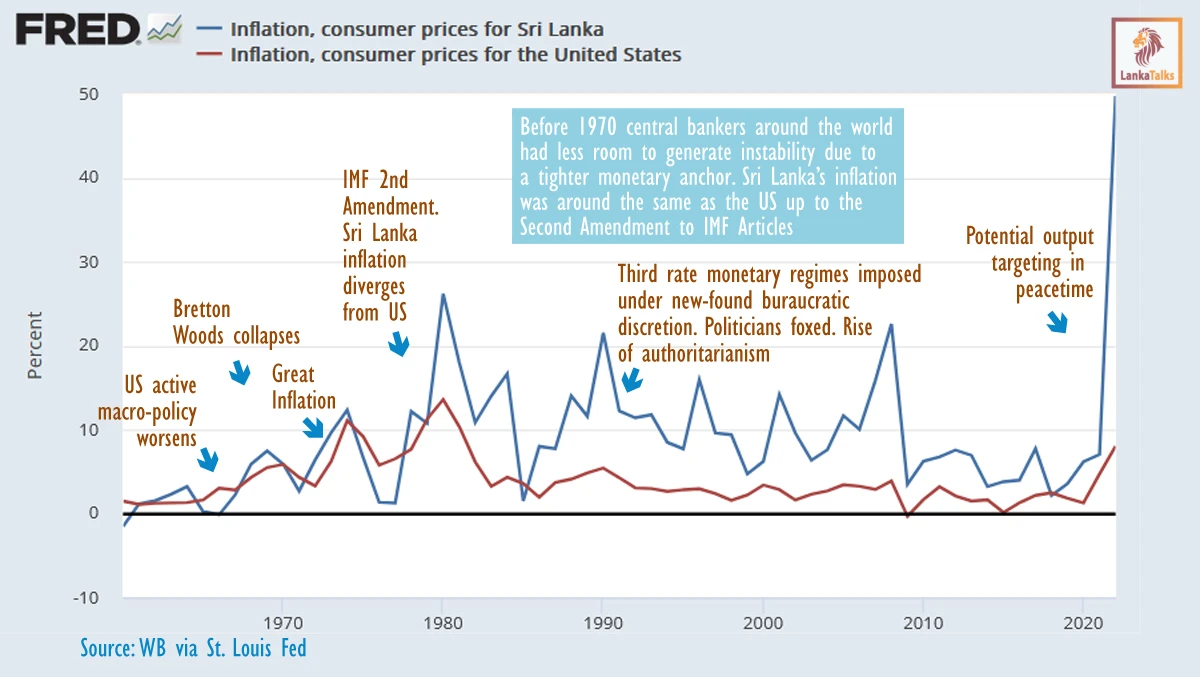

Sri Lanka’s inflation started to diverge from that of the US in the 1980s, after the IMF’s second amendment to its articles, when the rupee started to depreciate rapidly.

Current high inflation came after ‘exchange rate as the first line of defence’, which critics say allows a central bank to escape accountability for flaws in its operating framework, such as running inflation targeting frameworks without a floating exchange rate, or sterilizing reserve sales with inflationary open market operations.

When Wijewardene was in the central bank and the country was grappling with a war, there was no belief that inflation rather than stability helped growth. At the time pressure to inflate came from macro-economists in the Treasury who believed in Keynesian stimulus.

source: Economy Next